“Ohh, no? I think it’s way to early to say that. I think we’ve seen fantastic behavior from the public that has spared us the horror of the spike of the disease, but it’s just turned it into a marathon”

“So we can’t let our guard down.”

“Absolutely not. Not unless we want to start looking like… New York.”

Herman Cain, Former C.E.O. and Presidential Candidate, Dies at 74

Mr. Cain sought the 2012 Republican nomination and became an early supporter of Donald Trump’s 2016 bid. He had been hospitalized with the coronavirus.

He attended President Trump’s rally in Tulsa, Okla., last month and tested positive for the coronavirus shortly after.

(This is not financial advice. Continue to seek the counsel of qualified investment professionals to make level-headed and rational decisions that are reasonable for your personal goals)

I have recently come across something quite significant in my daily reading, to which the implications are so dire that I haven’t even finished processing them myself:

The U.S. financial system could be on the cusp of calamity. This time, we might not be able to save it.

I’m not really sure what’s going on here, but as they say:

.

History doesn’t repeat itself, but it often rhymes.

.

I hope to extend this post with a more detailed write-up as the full picture becomes more clear to me.

Matt’s Edit:

I should firstly clarify that overall this is a topic which I do not have terribly much knowledge of or experience with.

That being said, consensus seems to point towards American banks being in relatively decent shape under strains (best and worst case) that are currently thought as possible to occur:

So are too-big-to-fail banks really safer? The latest stress tests conducted by the Federal Reserve suggest the answer in America is “yes”

…

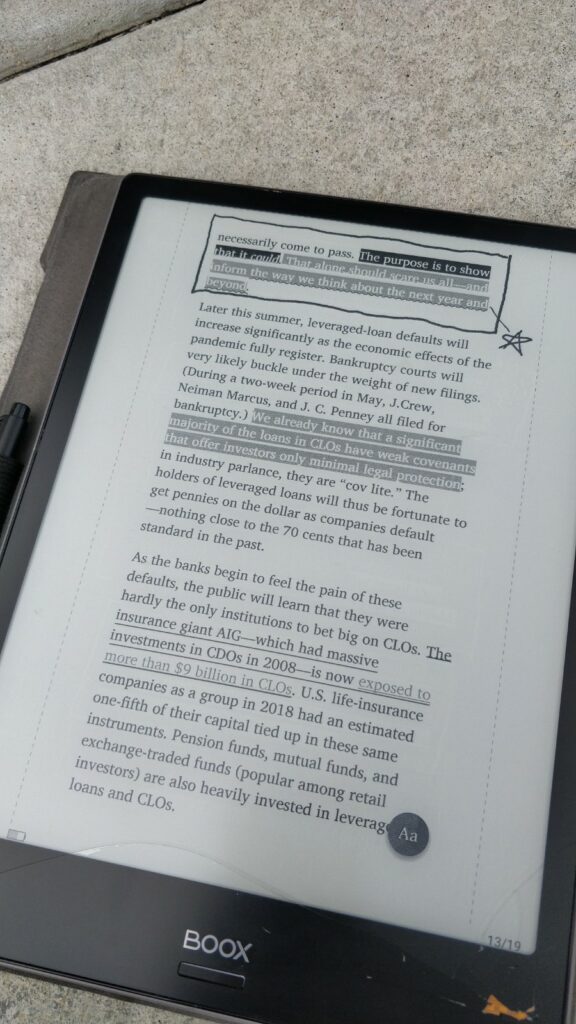

In a pessimistic “U-shape” scenario, in which the economy faces prolonged social distancing and repeated outbreaks of the virus, the Fed reckons that banks would face total losses of over $700n on their collective loan book.

…

Happily, the Fed concludes, in this U-shape scenario the banking system’s total core-capital ratio would fall from the present 12% to a still-passable 8%

This is certainly good news. I do not know enough about banking or finance however to comment if the dirth of unseen systemic issues this time around could still pose a greater risk than anticipated, as it did in ’08 (not the “known knowns”, but the “known unknowns”). The premise of this article from The Atlantic is still somewhat troubling to me.

Most significant movie scene of the decade. (And not just because it has Margot Robbie in a bubble bath)

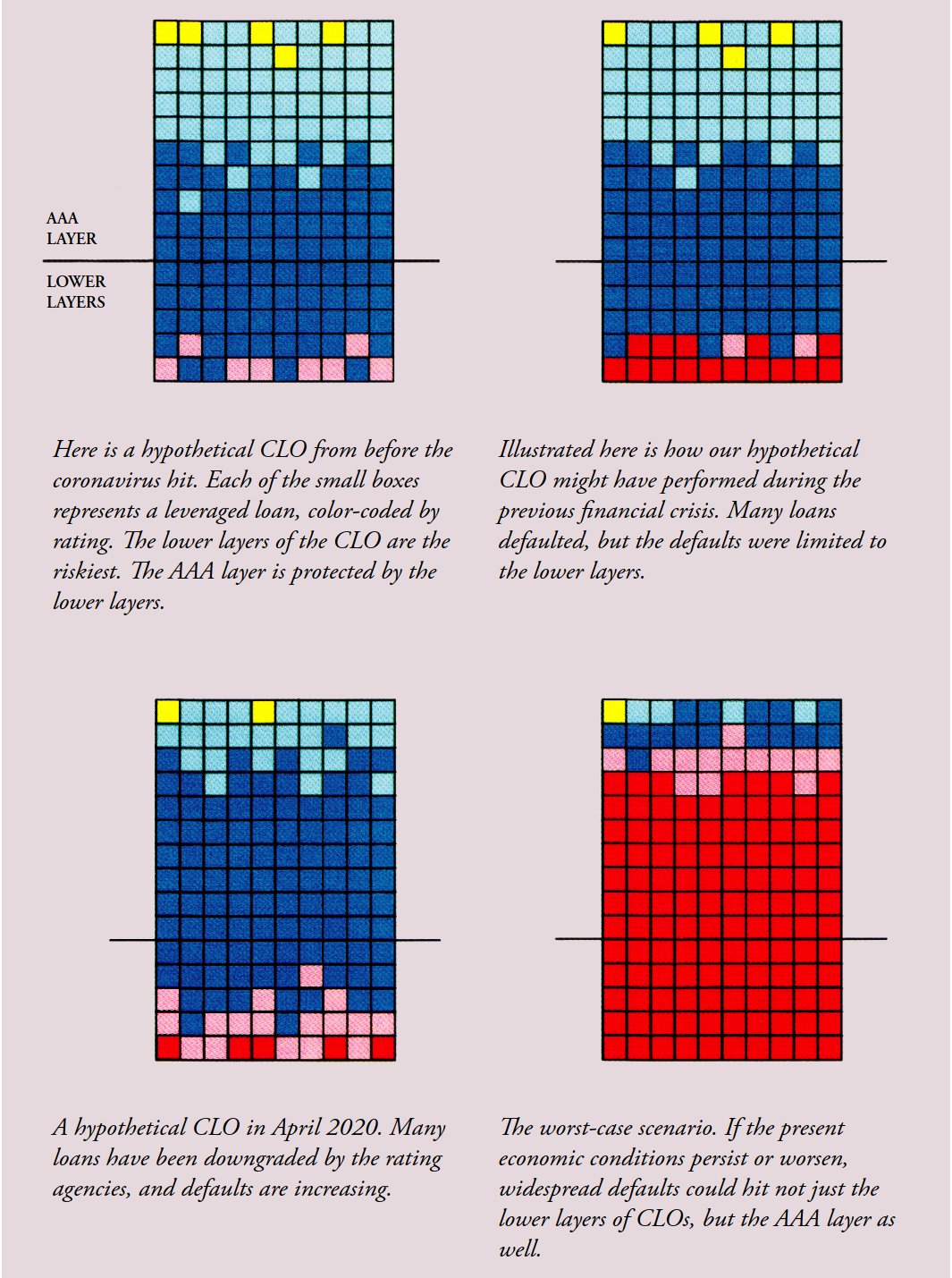

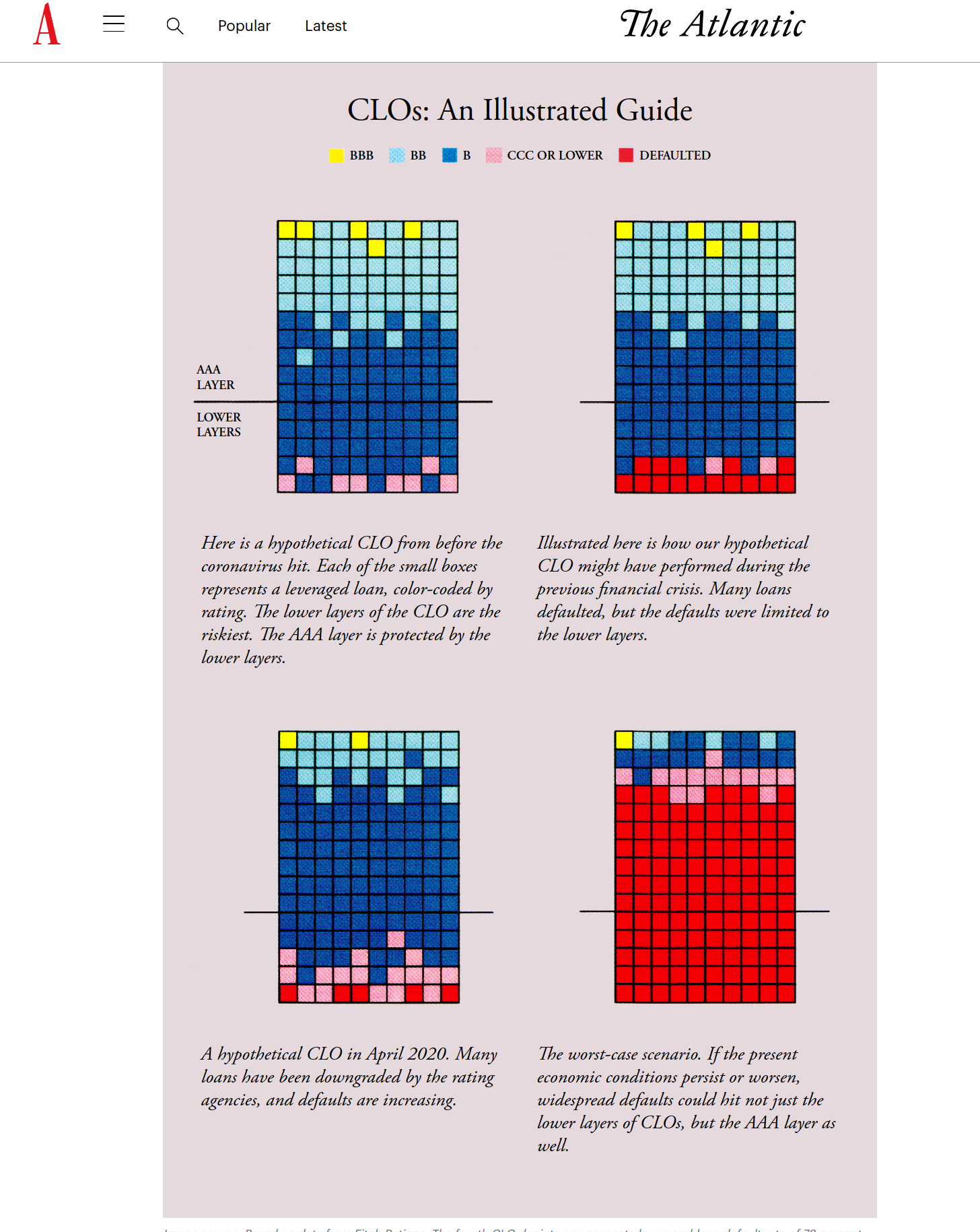

When you hear “subprime” think: ‘Shit’.

[Margot’s words, not mine.]

Also (for this time around), When you hear C, CCC, B, or “BBB“, think: ‘Shit‘

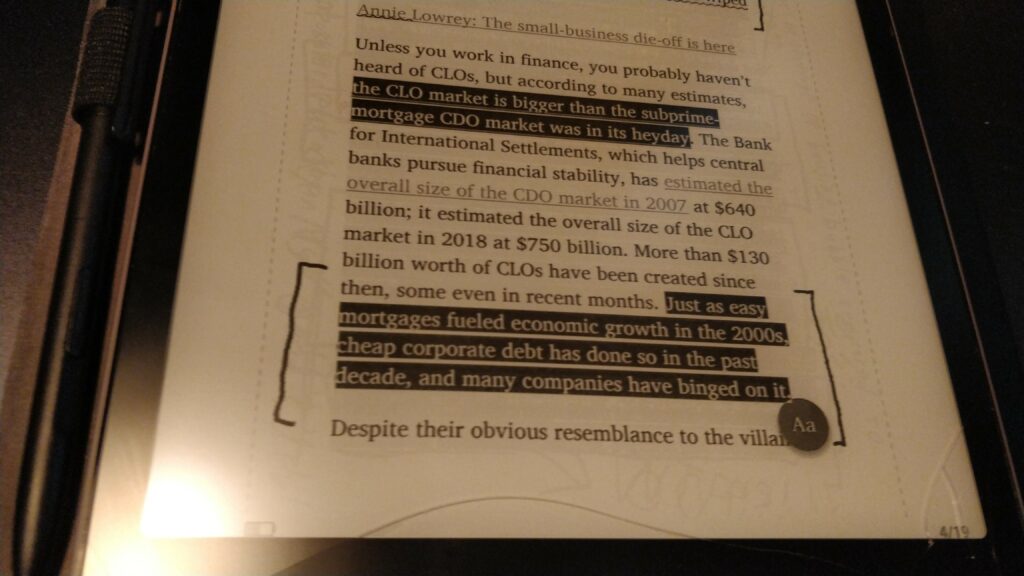

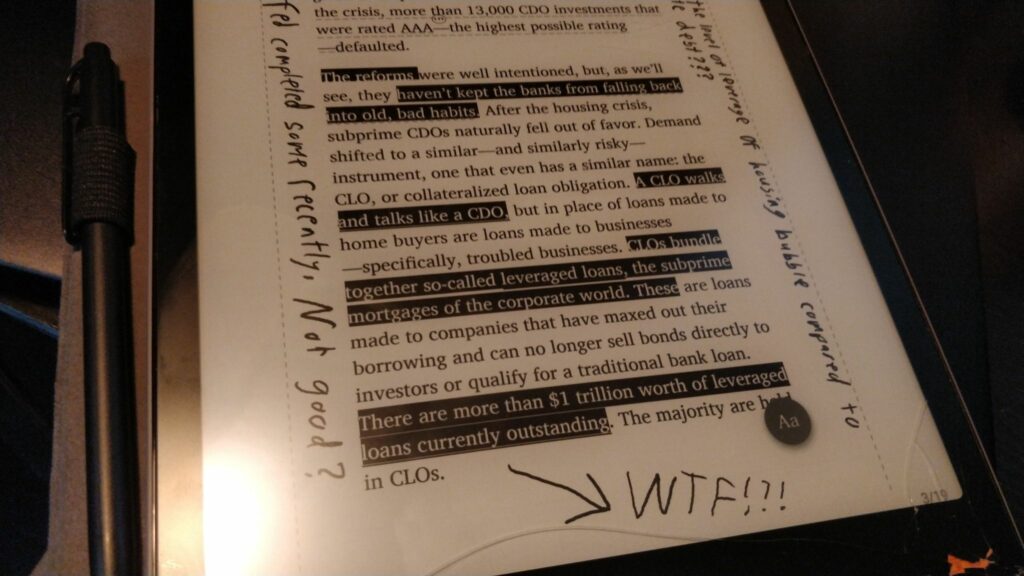

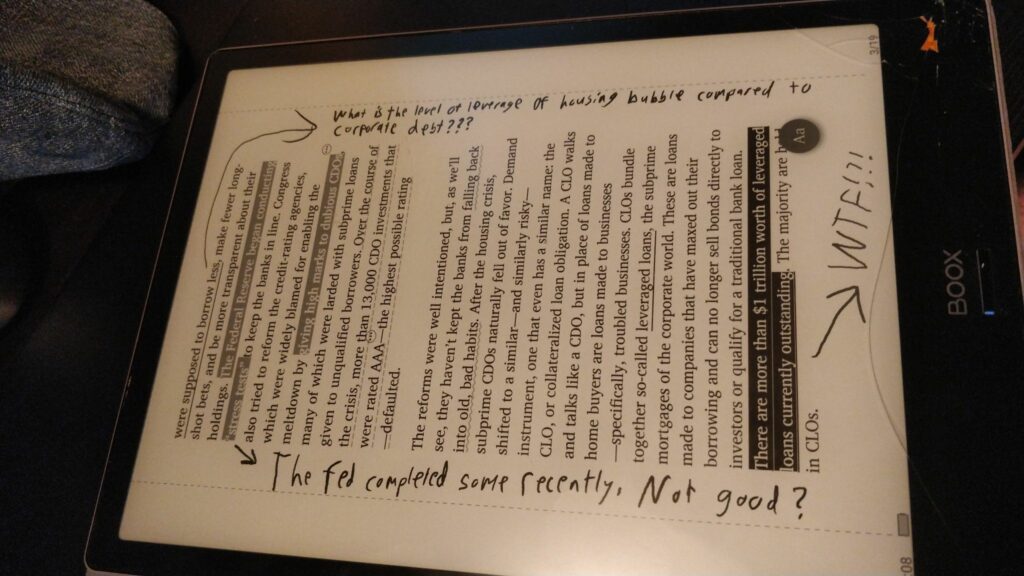

“””There are More than $1 Trillion worth of leveraged loans currently outstanding.””” “””The Majority are held in CLOs”””

Our nation’s brightest over at AIG are at it again:

We can all laugh in hindsight about how foolish Goldman was here and how smart Michael Bury was, but in reality, who was fulfilling those credit-default swaps on the back end?

There is another reason for the popularity of fake news on the political right (“Return of the paranoid style”, June 6th). It is the double standards found in most of the media’s reporting. This conservative complaint is not entirely a myth. Take covid-19. Widespread demonstrations in early May by right-wing anti-lockdown protesters were depicted by the media as selfish and menacing acts that would result in the virus being spread. Yet the protests that erupted over George Floyd’s horrific death just a few weeks later were praised by the same media. The same Democratic governors who supported lockdown and prevented businesses from reopening even participated in the marches.

One group of experts on infectious diseases, whom I presume supported the lockdowns, penned a letter with over 1,200 signatures stating that the protests were necessary to fight “white supremacy”. It is hard to imagine that these experts would support street demonstrations by conservatives in the middle of a pandemic. Commentators on the right had a field day pointing out the hypocrisy. A politicised scientific and medical community is deeply worrying because it boosts the argument on the far right that supposedly unbiased science and scholarship are a sham.

Matt’s Note: Unbiased science and scholarship are indeed important. While I do my best to be objective in my analyses, I can readily admit I’m somewhat biased and that comes out in my writing.

Please seek out other resources (they do a much better job and have a much better idea of what they’re talking about than I, anyways) if this is important to you.

The COVID-19 pandemic pushed economies into a Great Lockdown, which helped contain the virus and save lives, but also triggered the worst recession since the Great Depression. Over 75 percent of countries are now reopening at the same time as the pandemic is intensifying in many emerging market and developing economies. Several countries have started to recover. However, in the absence of a medical solution, the strength of the recovery is highly uncertain and the impact on sectors and countries uneven.

We are now projecting a deeper recession in 2020 and a slower recovery in 2021.

Compared to our April World Economic Outlook forecast, we are now projecting a deeper recession in 2020 and a slower recovery in 2021. Global output is projected to decline by -4.9 percent in 2020, 1.9 percentage points below our April forecast, followed by a partial recovery, with growth at 5.4 percent in 2021.

I am not a doctor. Please follow the advice of your country’s public health officials (or, if they are being subverted and are hampered in their data collection and dissemination of information to the public due to idiotic political pressure, please also consult the WHO and reputable public institutions)

With certain states loosening restrictions — and others partially in lockdown — there’s a lot of widespread confusion about COVID-19 risks. We talk with University of Minnesota epidemiologist Michael Osterholm about the safety concerns in terms of protests, indoor gatherings, touching surfaces, and why the antibody test is so flawed.

I think right now, most of the world — not just the United States, but most of the world — is quite confused about what to do or why to do it. And what I mean by that is, is that already I think we’ve seen pandemic fatigue set in, in the United States. Right around Memorial Day, the country was ready to say, ”We’re done with this. We’re unlocking. We’re going to no longer do the kind of physical distancing that’s been recommended. We should reopen the economy. Let’s let the cards fall where they may.” And I think to myself, wow, that’s what’s happened after 5% of the population has been infected. How might we ever get a population to do what it needs to do to reduce transmission to hopefully get to that vaccine before the disease gets us to that 60 or 70% level.

And I think to myself, wow, that’s what’s happened after 5% of the population has been infected. How might we ever get a population to do what it needs to do to reduce transmission to hopefully get to that vaccine before the disease gets us to that 60 or 70% level.

That’s going to be months and months. This is not what is going to last for a few more weeks. And if you look at influenza pandemics, they all did last for years, not for just a couple of months. And so I think that that’s the challenge we have today is helping people understand: We’ve got to figure out how to live with this virus as much as we’ve had to painfully understand how to die with this virus.

@nprfreshair Excellent interview today with infectious disease expert Michael Osterholm.

Regarding surface cleaners causing antibiotic resistance: This is a common misconception.

I believe the worry with antibiotics is that the good ones that…

Lewis was correct. In 1918 an influenza virus emerged—probably in the United States—that would spread around the world, and one of its earli- est appearances in lethal form came in Philadelphia. Before that world- wide pandemic faded away in 1920, it would kill more people than any other outbreak of disease in human history. Plague in the 1300s killed a far larger proportion of the population—more than one-quarter of Europe— but in raw numbers influenza killed more than plague then, more than AIDS today. The lowest estimate of the pandemic’s worldwide death toll is twenty- one million, in a world with a population less than one-third today’s. That estimate comes from a contemporary study of the disease and newspapers have often cited it since, but it is almost certainly wrong. Epi- demiologists today estimate that influenza likely caused at least fifty mil- lion deaths worldwide, and possibly as many as one hundred million. Yet even that number understates the horror of the disease, a horror contained in other data. Normally influenza chiefly kills the elderly and infants, but in the 1918 pandemic roughly half of those who died were young men and women in the prime of their life, in their twenties and thirties. Harvey Cushing, then a brilliant young surgeon who would go on to great fame—and who himself fell desperately ill with influenza and never fully recovered from what was likely a complication—would call these victims “doubly dead in that they died so young.”

One cannot know with certainty, but if the upper estimate of the death toll is true, as many as 8 to 10 percent of all young adults then living may have been killed by the virus.

…perhaps two-thirds of the deaths occurred in a period of twenty-four weeks, and more than half of those deaths occurred in even less time, from mid-September to early December 1918.

Influenza killed more people in a year than the Black Death of the Middle Ages killed in a century; it killed more people in twenty-four weeks than AIDS has killed in twenty-four years.

One cannot know with certainty, but if the upper estimate of the death toll is true as many as 8 to 10 percent of all young adults then liv- ing may have been killed by the virus. And they died with extraordinary ferocity and speed. Although the influenza pandemic stretched over two years, perhaps two-thirds of the deaths occurred in a period of twenty-four weeks, and more than half of those deaths occurred in even less time, from mid-September to early December 1918. Influenza killed more people in a year than the Black Death of the Middle Ages killed in a century; it killed more people in twenty-four weeks than AIDS has killed in twenty-four years. The influenza pandemic resembled both of those scourges in other ways also. Like AIDS, it killed those with the most to live for. And as priests had done in the bubonic plague, in 1918, even in Philadelphia, as modern a city as existed in the world, priests would drive horse-drawn wagons down the streets, calling upon those behind doors shut tight in terror to bring out their dead.

Yet the story of the 1918 influenza virus is not simply one of havoc, death, and desolation, of a society fighting a war against nature superimposed on a war against another human society. It is also a story of science, of discovery, of how one thinks, and of how one changes the way one thinks, of how amidst near-utter chaos a few men sought the coolness of contemplation, the utter calm that precedes not philosophizing but grim, determined action. For the influenza pandemic that erupted in 1918 was the first great collision between nature and modern science. It was the first great colli- sion between a natural force and a society that included individuals who refused either to submit to that force or to simply call upon divine inter- vention to save themselves from it, individuals who instead were deter- mined to confront this force directly, with a developing technology and with their minds. In the United States, the story is particularly one of a handful of extraordinary people, of whom Paul Lewis is one. These were men and some very few women who, far from being backward, had already devel- oped the fundamental science upon which much of today’s medicine is based. They had already developed vaccines and antitoxins and tech- niques still in use. They had already pushed, in some cases, close to the edge of knowledge today.

The Great War had brought Paul Lewis into the navy in 1918 as a lieutenant commander, but he never seemed quite at ease when in his uniform. It never seemed to fit quite right, or to sit quite right, and he was often flustered and failed to respond properly when sailors saluted him. Yet he was every bit a warrior, and he hunted death. When he found it he confronted it, challenged it, tried to pin it in place like a lepidopterist pinning down a butterfly, so he could then dis- sect it piece by piece, analyze it, and find a way to confound it. He did so often enough that the risks he took became routine. Still, death had never appeared to him as it did now, in mid-September 1918. Row after row of men confronted him in the hospital ward, many of them bloody and dying in some new and awful way.

Most of the blood had come from nosebleeds. A few sailors had coughed the blood up. Others had bled from their ears. Some coughed so hard that autopsies would later show they had torn apart abdominal muscles and rib cartilage. And many of the men writhed in agony or delirium; nearly all those able to communicate complained of headache, as if someone were hammering a wedge into their skulls just behind the eyes, and body aches so intense they felt like bones breaking. A few were vomiting. Finally the skin of some of the sailors had turned unusual colors; some showed just a tinge of blue around their lips or finger-tips, but a few looked so dark one could not tell easily if they were Caucasian or Negro. They looked almost black.

The clinicians now looked to him to explain the violent symptoms these sailors presented. The blood that covered so many of them did not come from wounds, at least not from steel or explosives that had torn away limbs. Most of the blood had come from nosebleeds. A few sailors had coughed the blood up. Others had bled from their ears. Some coughed so hard that autopsies would later show they had torn apart abdominal muscles and rib cartilage. And many of the men writhed in agony or delirium; nearly all those able to communicate complained of headache, as if someone were hammering a wedge into their skulls just behind the eyes, and body aches so intense they felt like bones breaking. A few were vomiting. Finally the skin of some of the sailors had turned unusual colors; some showed just a tinge of blue around their lips or finger- tips, but a few looked so dark one could not tell easily if they were Cau- casian or Negro. They looked almost black. Only once had Lewis seen a disease that in any way resembled this. Two months earlier, members of the crew of a British ship had been taken by ambulance from a sealed dock to another Philadelphia hospital and placed in isolation. There many of that crew had died. At autopsy their lungs had resembled those of men who had died from poison gas or pneumonic plague, a more virulent form of bubonic plague. Whatever those crewmen had had, it had not spread. No one else had gotten sick. But the men in the wards now not only puzzled Lewis. They had to have chilled him with fear also, fear both for himself and and for what this disease could do. For whatever was attacking these sailors was not only spreading, it was spreading explosively.

For whatever was attacking these sailors was not only spreading, it was spreading explosively.

And it was spreading despite a well-planned, concerted effort to contain it.

And it was spreading despite a well-planned, concerted effort to contain it. This same disease had erupted ten days earlier at a navy facility in Boston. Lieutenant Commander Milton Rosenau at the Chelsea Naval Hospital there had certainly communicated to Lewis, whom he knew well, about it. Rosenau too was a scientist who had chosen to leave a Harvard professorship for the navy when the United States entered the war, and his textbook on public health was called “The Bible” by both army and navy military doctors. Philadelphia navy authorities had taken Rosenau’s warnings seriously, especially since a detachment of sailors had just arrived from Boston, and they had made preparations to isolate any ill sailors should an outbreak occur. They had been confident that isolation would control it. Yet four days after that Boston detachment arrived, nineteen sailors in Philadelphia were hospitalized with what looked like the same disease. Despite their immediate isolation and that of everyone with whom they had had contact, eighty-seven sailors were hospitalized the next day. They and their contacts were again isolated. But two days later, six hundred men were hospitalized with this strange disease. The hospital ran out of empty beds, and hospital staff began falling ill. The navy then began sending hundreds more sick sailors to a civilian hospital. And sailors and civilian workers were moving constantly between the city and navy facilities, as they had in Boston. Meanwhile, personnel from Boston, and now Philadelphia, had been and were being sent throughout the country as well.

Matt’s Note: While I have not thoroughly vetted this source, various corroborating viewpoints from other varied sources lead me to conclude that there is no pressing reason to doubt it:

Various surveys, economic growth projections, and market risk indicators portray a short period (through mid-2020) of substantial U.S. economic decline, followed by a sustained significant economic rebound and then financial system stability for the foreseeable future.

However, there are various indications – many of which have been discussed on this site – that this very widely-held consensus is in many ways incorrect. There are many exceedingly problematical financial conditions that have existed prior to 2020, and continue to exist. As well, numerous economic dynamics continue to be exceedingly worrisome and many economic indicators have portrayed facets of weak growth or outright decline prior to 2020.

Of paramount importance is the resulting level of risk and the future economic implications.

From an “all things considered” standpoint, I continue to believe the overall level of risk remains at a fantastic level – one that is far greater than that experienced at any time in the history of the United States.

Cumulatively, these highly problematical conditions will lead to future upheaval. The extent of the resolution of these problematical conditions will determine the ongoing viability of the financial system and economy as well as the resultant quality of living.

My analyses continues to indicate that the growing level of financial danger will lead to the next stock market crash that will also involve (as seen in 2008) various other markets as well. Key attributes of this next crash is its outsized magnitude (when viewed from an ultra-long term historical perspective) and the resulting economic impact. This next financial crash is of tremendous concern, as my analyses indicate it will lead to a Super Depression – i.e. an economy characterized by deeply embedded, highly complex, and difficult-to-solve problems.

ANDY SERWER: What do you think about the president’s campaign to lobby the Fed to lower rates or keep rates low?

CHARLIE MUNGER: Well, I think presidents have always done this. If you’re a politician in a democracy, of course you want people to earn money and spend it. And of course, that’s not a good idea. The best example probably in the whole world is Singapore, which has zero debt and never prints money and spends it. And it’s one of the most successful places on earth. I wish we were like that, but there’s only one Singapore.

ANDY SERWER: Well, some people now say that federal debt is not a problem at all.

CHARLIE MUNGER: Well, if you believe that, you believe in the tooth fairy. Because then we don’t have to have any more taxes ever. We’ll just print money and live happily ever after. It obviously won’t work. There comes a point when printing money is counterproductive.

ANDY SERWER: Are we at that point? Are you concerned?

CHARLIE MUNGER: No, I don’t think we are at that point. But nobody knew where the point was going to come. And we don’t know now. None of these people who are so pompously sure of things, because we all want reassurances, so they provide it. But nobody really knows how much of this is too much.

NPR Here & Now‘s Jeremy Hobson speaks with Dr. Michael Osterholm, director of the Center for Infectious Disease Research at the University of Minnesota and author of several books on killer germs.

Infectious disease expert Michael Osterholm, who has been warning for a decade and a half about the possibility of a global pandemic, said the coronavirus we’re fighting is at least as infectious as the one that killed an estimated 50 million people in the 1918 flu worldwide outbreak.

He said we’re only in the second inning of a nine-inning contest, with the possibility of as many as 800,000 deaths or more in the US over the next 18 months.

Osterholm also pointed to a shortage of chemical reagents that are necessary for widespread testing for the virus and said that the CDC’s low public profile in this pandemic in the United States has been a “tragedy.”

He decried the lack of a national long-term strategy for the pandemic and noted that there are real questions about the efficacy of the antibody tests that are being developed to detect if people have been exposed to the virus.

…

For example, everybody wants to do widescale coronavirus testing today. Talking heads without any experience in testing declare, “We’ll test millions of people each week, and then we’ll know who is infected and can follow up.” Very few people realize that the testing community in this country can’t do that. We don’t have adequate international manufacturing capacity and supply chains for reagents, the chemicals needed to run these tests.

The reagent capability — meaning securing those chemicals that are key for running many of these tests, whether you’re testing for virus or antibody — before the pandemic was more or less, adequately supported by a “garden hose of production.” Then Covid-19 came along and the Asian countries, specifically China, demanded a major increase in reagent supplies.

Finally, the whole world caught the pandemic, and now there are billions of people who need to be tested. We need a firehose to meet that demand but we can’t build reagent manufacturing facilities overnight. I urge that whatever we do going forward has to be based on reality. We’re not going to test your way out of this thing when we don’t have tests.

…

This virus could be in the air around infected people. It could be the same air we share and breathe. The more times you go into public spaces, the greater the likelihood you’re going to swap some air with somebody who has the virus and doesn’t even know it. Again, we have to be honest about that.

Does that mean you shouldn’t go to the grocery store? Well, I would say if you’re a person of high risk for a serious disease outcome, you should do everything you can to find a way to get those groceries delivered to you, even left outside your front door where you can go pick them up and not have to have contact with someone.

Now, for others who say, “Well, you know what? I’m at a relatively low risk of having a serious outcome if I do get infected,” you still have to think about whether you might be transmitting that infection to others. I think we have to be more honest and just say that, yes, breathing someone else’s air is going to put you at risk. On any one given day, how big of a risk is that? I don’t know.

We can’t stop living life. We have to move forward. But we must do so while thinking about how to get people back into society in a way that is thoughtful and takes into account every possible option to make sure people don’t get seriously ill and don’t subsequently die.

(This is not financial advice. I have no idea what I’m talking about on this topic anyways.)

⚠️: This article reflects that Matt’s opinion aligns with the following author on seeking alpha, without a full pretense of certainty or full supported basis in readily observable facts as with other postings:

Fed and Treasury stimulus will not be able to prevent massive losses of income, production and wealth in the economy.

Despite stimulus, vast numbers of businesses in high employment industries will disappear and/or take many years to recover.

No V-Shaped recovery. It will take years for former levels of production to be reestablished in many industries. It will take nearly a decade for a return to full employment.

There’s no free lunch. Massive increases in public and private debt burdens will impose enormous impediments on future growth.

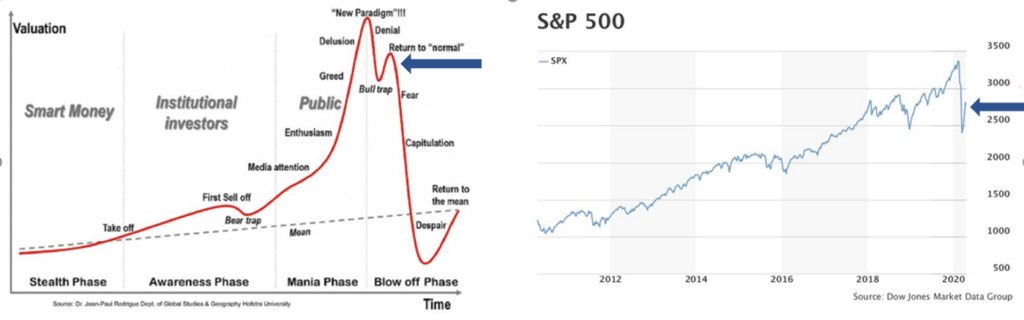

Since the recent low of 2237.40 registered on March 23, the S&P 500 index has staged a major counter-trend rally gain of 24.69%, as of April 9. This includes a gain of 11.23% in the past week. Although there were several technical factors and news catalysts that have contributed to this massive counter-trend rally, perhaps the most important critical factor has been expectations and announcements regarding unprecedented measures by the US Treasury and the US Federal Reserve to inject massive amounts of fiscal and monetary stimulus into the US economy and financial markets.

In this article I will explain why the combined measures by the US Treasury and Fed will not be enough to prevent massive and long-lasting losses of national income, production and wealth. In particular, I will show that in the context of their inability to prevent a massive and prolonged economic crisis that will extend well into 2021, US Treasury and Fed stimulus measures will not ultimately prevent the occurrence of another massive leg down in US equities. Indeed, after the current counter-trend rally fizzles out and the primary bear market trend resumes, in the course of the next leg down, US equity prices will collapse significantly below recent lows and establish a bottom somewhere between the range of approximately 1900 and 1500 on the S&P 500 index. The eventual recovery from this intermediate-term bottom will most likely be prolonged and painful (as opposed to V-shaped), with potential – depending on various developments – for occurrence of yet another major leg down to even lower levels.

The Economic Backdrop

The Unites States is barely in the initial stages of one of the most devastating economic crises in the nation’s history. Certainly, the forthcoming economic crisis will the most severe since the Great Depression…

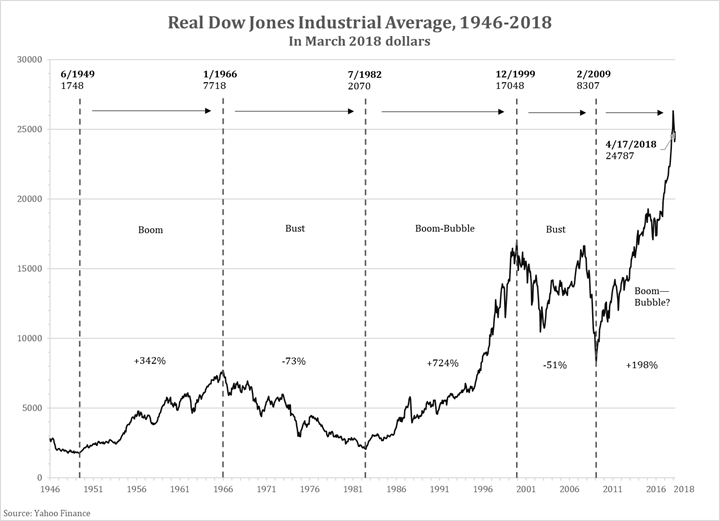

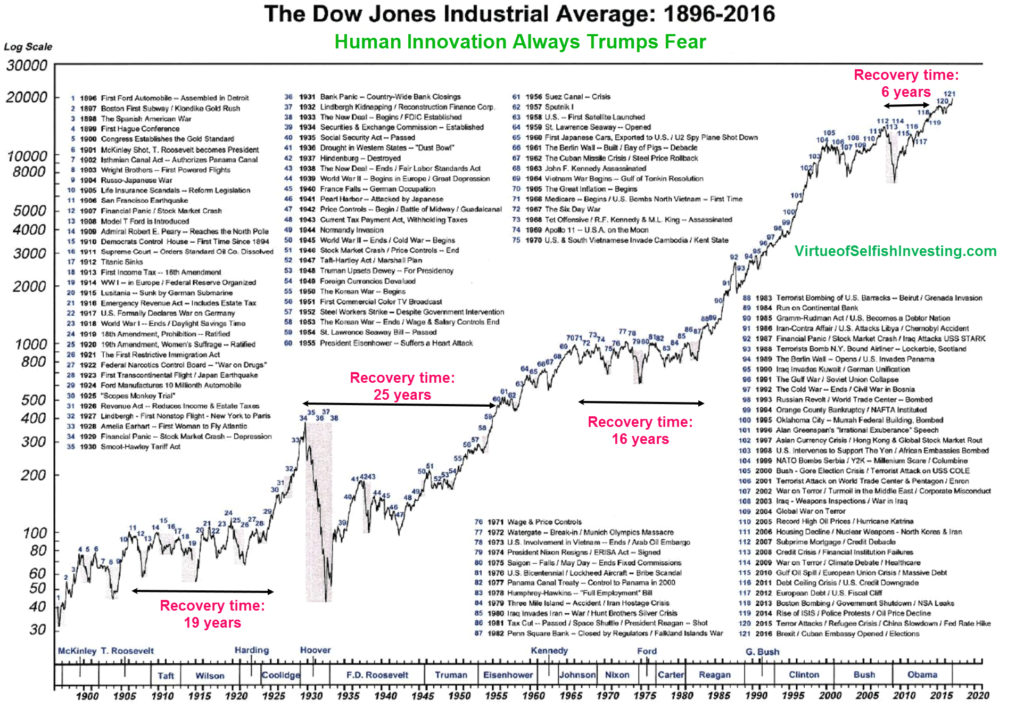

For a fun history lesson, take a look at items 34, 35, and 36 on this chart in the great depression era The Great Depression was started by a myriad of issues, but among those:

A runaway equities bubble due to even common folk trading on margin (loans)

Federal reserve interest rates were hiked up at the absolute worst time (borrowing more expensive)

(36) Nationwide run on the banks vastly and quickly reducing the money supply

And of course, (35) the devastating Smoot–Hawley tariff act, to which some have compared Trump’s recent protectionary tariffs

(A ludicrous bill where every state tacked on “me too” tariffs for their particular industry, the sum of which devastated the entire economy)

[Congress soon after forbade themselves from being able to pass tariffs, “like a kid in a candy store”, hence why the presidential executive branch controls them]

This is not entirely scientific, but it’s a question worth asking:

First, let us get our numbers straight. Someone told me the market declined 35% but already was up 25% so it’s now really only down 9%, barely enough to call it a correction.

I know that most SA readers are experienced enough to know this is not quite accurate. I told this gentlemen what you would expect: “If you have $100 invested in something and it declines 34%, how many ‘dollars’ does that leave you with?”

“$66.”

“And what does a 25% rally take you back to?”

“Is this a trick question? $66 plus $25 is $91. Like I said, just down 9%.”

“Not exactly. Since you only have $66 remaining, the 25% rebound is on $66, not $100. Therefore 25% of $66 is $16.50, so you have rebounded to $82.50.”

He eyed me skeptically and said, “You Wall Street guys can twist anything around.”

For the record, I’m not a Wall Street guy. I run my business from the shores of Lake Tahoe in the no income tax, more ranchers than gamblers corner of Nevada, a state where our legislature meets only every other year. The skeleton in my closet demands I tell you I once did work on Wall Street but got out of there as soon as I could.

My biggest concern about this rally: It has little support beyond what was being supported before the decline. Let me explain.

Leadership before the decline rested with the FANGMAN stocks. Leadership in this rally out of the decline has been the same. Investors did not take the time or give the attention to those fine companies that might have gotten ahead of themselves in price prior to the decline and now provide the opportunity to diversify away from FANGMAN with perhaps a greater capital gain potential. Nope, many are sticking with what worked before, ever and always.

That may yet prove to be a brilliant move, but there are those of us who see the rush back to FANGMAN as reminiscent of the Nifty Fifty of the 70s. This was a period in which the leadership got narrower and narrower until institutions and individuals alike were pretty much buying the same thing – only the 50 anointed companies seen as being the biggest and the best.

That did not end well. When the armor cracked, as it always will in one place or another, the rush to exit was brutal.

Buffett’s advice in general: forget the pundits (like me), charts and the manic depressive traders, buy (not necessarily now, but you’re free to if you want!) a cross-section of America (i.e. stock in solid businesses through ETF’s, etc.) and forget about it [very long term]:

https://www.youtube.com/watch?v=MDYJWIWsgBA

2020-05-02 (May 2nd) From Berkshire Hathaway (NYSE:BRK) 2020 Annual Meeting

Anomalies in Buffet’s trading behavior?

https://youtu.be/x25kzo9XldA

Created 2020-08-28 (August 28th)

Breaking down Buffett’s comments at Berkshire Hathaway 2020 Shareholder’s meeting:

2020-05-02 (May 2nd) From Berkshire Hathaway (NYSE:BRK) 2020 Annual Meeting

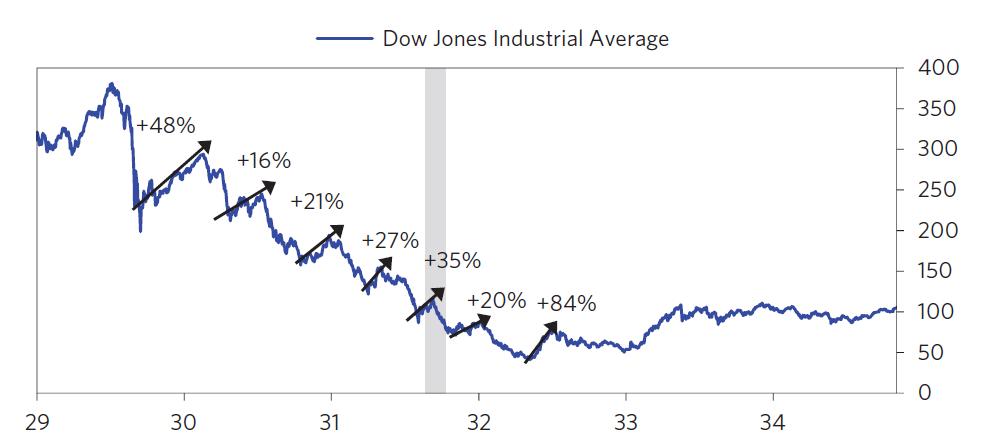

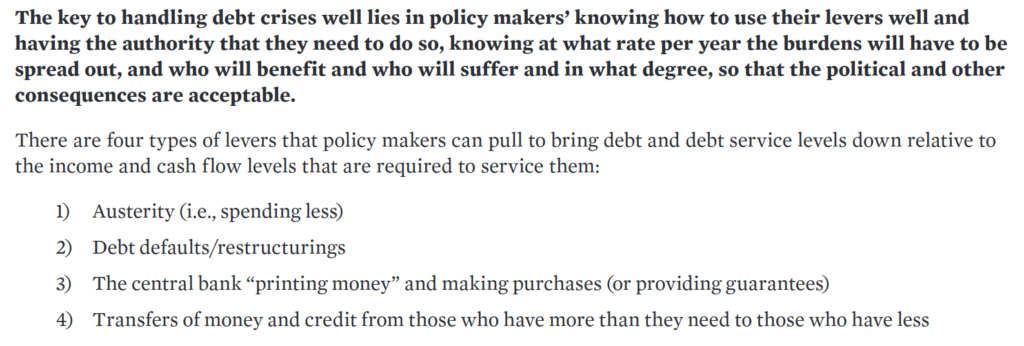

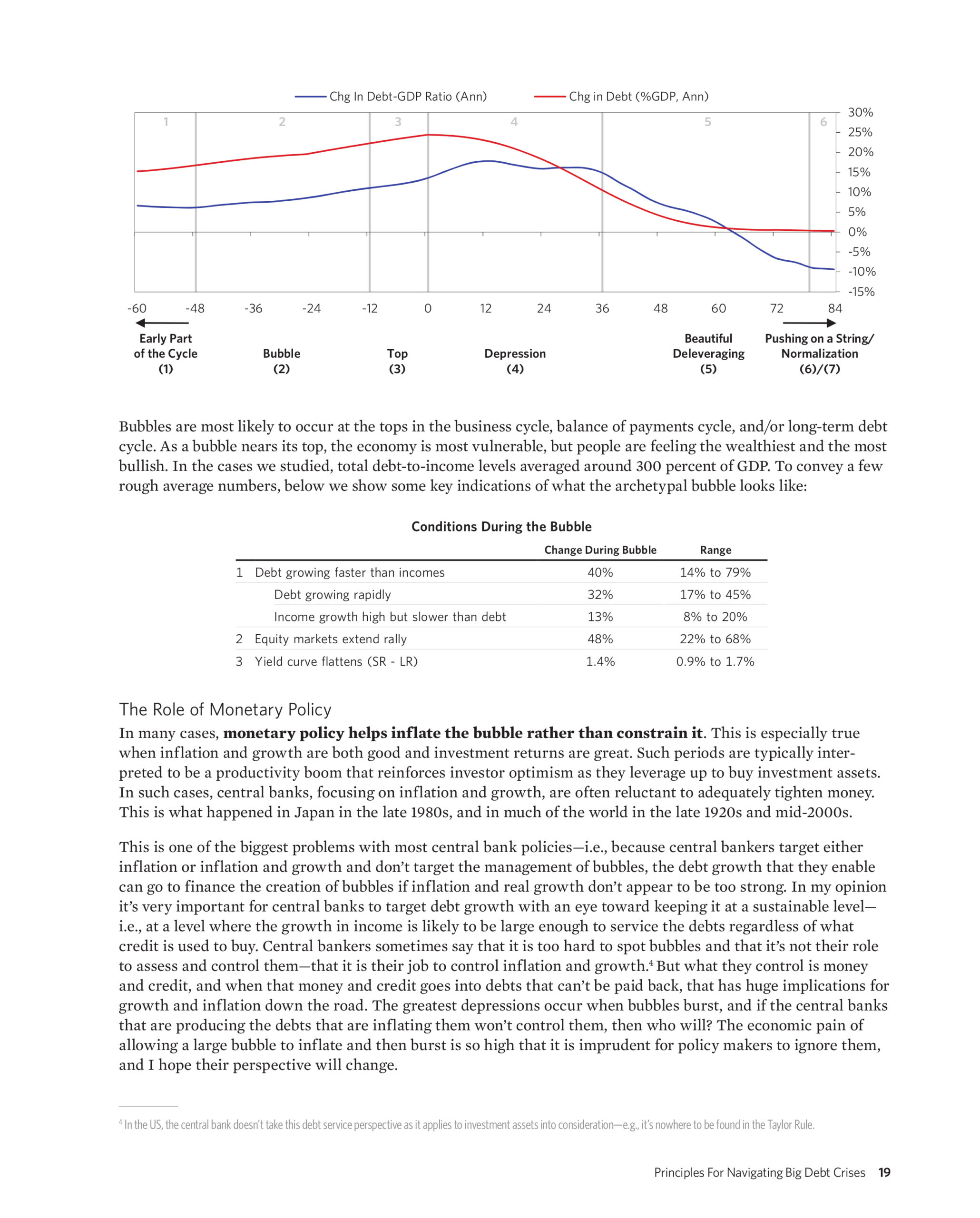

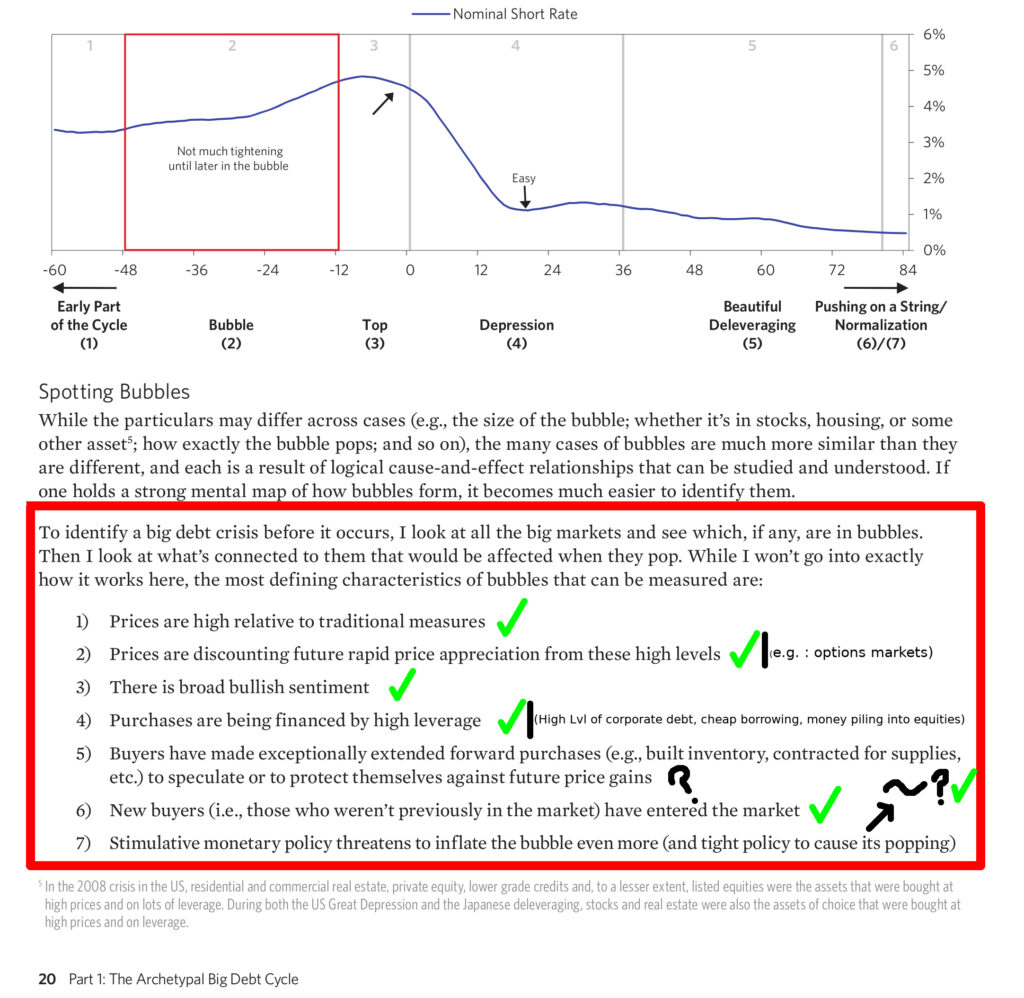

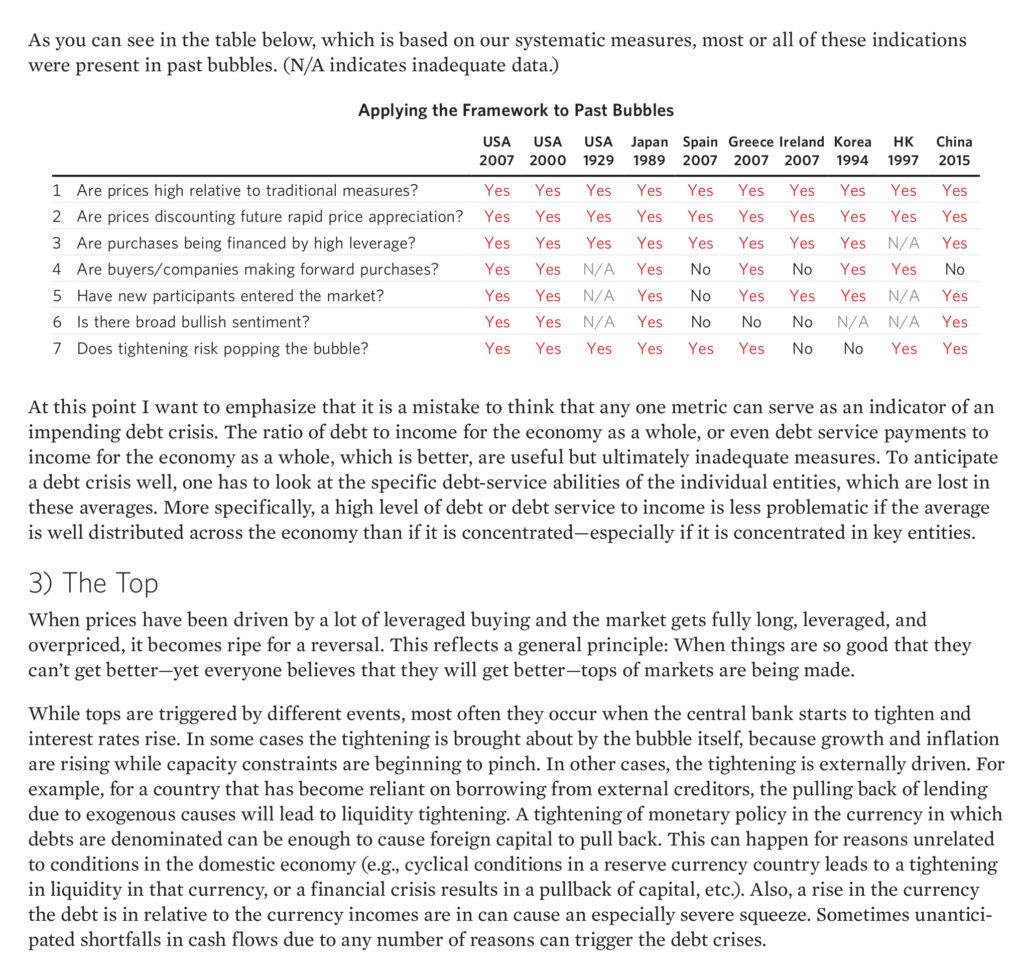

For those of you who have not read “Principles For Navigating Big Debt Crisis” by Ray Dalio, I highly recommend it. Especially the section on the 1930’s. Below is a snippet from his book showing the sharp rallies we had in the early 1930’s. Each one fueled by optimism on stimulus and the “worst is over” narrative.

Bubbles are most likely to occur at the tops in the business cycle, balance of payments cycle, and/or long-term debt cycle. As the bubble nears its top, the economy is most vulnerable, but people are feeling the wealthiest and the most bullish.

…

In many cases, monetary policy helps inflate the bubble rather than constrain it

Typically debt crises occur because debt and debt service costs rise faster than the incomes that are needed to service them, causing a deleveraging. While the central bank can alleviate typical debt crises by lowering real and nominal interest rates, severe debt crises (i.e., depressions) occur when this is no longer possible

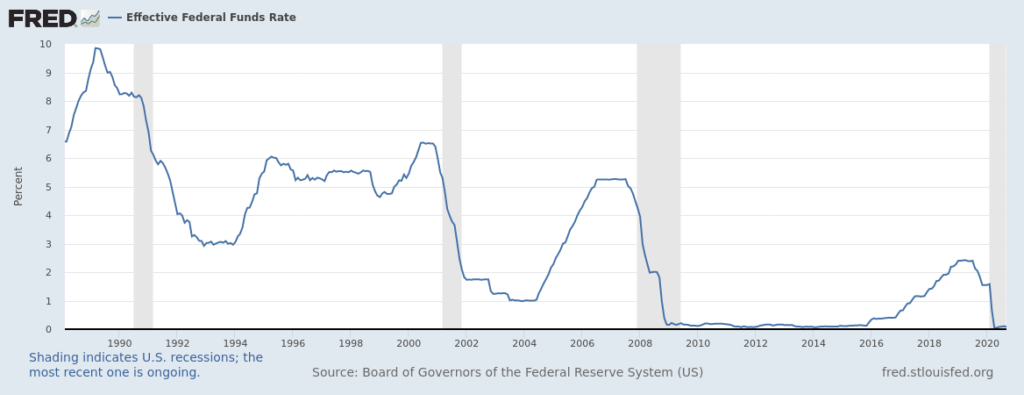

Effective Federal Funds Rate ~198X-2020 via Federal Reserve Bank of St. Louis Captured 2020-10-23

In the immediate post-bubble period, the wealth effect of asset price movements has a bigger impact on economic growth rates than monetary policy does. People tend to underestimate the size of this effect. In the early stages of a bubble bursting, when stock prices fall and earnings have not yet declined, people mistakenly judge the decline to be a buying opportunity and find stocks cheap in relation to both past earnings and expected earnings, failing to account for the amount of decline in earnings that is likely to result from what’s to come. But the reversal is self-reinforcing.

Some people mistakenly think that depressions are psychological: that investors move their money from riskier investments to safer ones (e.g., from stocks and high-yield lending to government bonds and cash) because they’re scared, and that the economy will be restored if they can only be coaxed into moving their money back into riskier investments.

This is wrong for two reasons: First, contrary to popular belief, the deleveraging dynamic is not primarily psychological. It is mostly driven by the supply and demand of, and the relationships between, credit, money, and goods and services—though psychology of course also does have an effect, especially in regard to the various players’ liquidity positions. Still, if everyone went to sleep and woke up with no memory of what had happened, we would be in the same position, because debtors’ obligations to deliver money would be too large relative to the money they are taking in. The government would still be faced with the same choices that would have the same consequences, and so on.

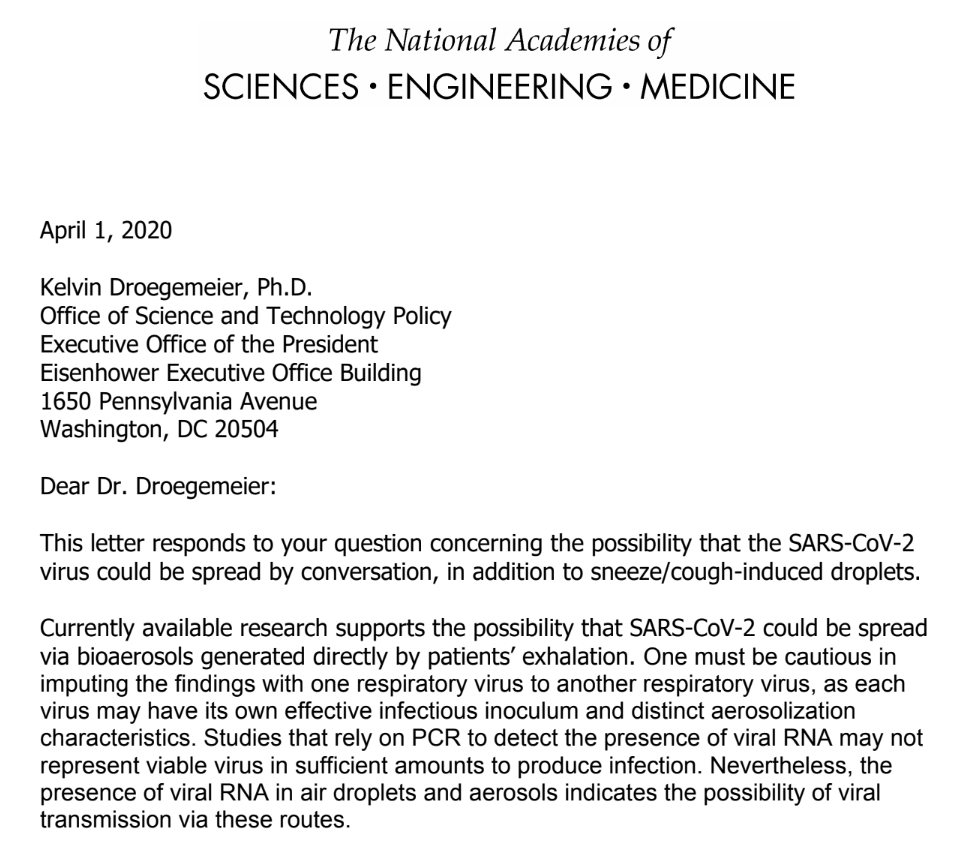

Harvey V. Fineberg, a noted researcher in the fields of health policy and medical decision making,

writes to Kelvin Droegemeier, who is currently serving as the Director of the Office of Science and Technology Policy and Acting Director of the National Science Foundation,

On the possibility of airborne, respiratory transmission of SARS-CoV-2:

(i.e. passive through talking, breathing, etc. aerosolized particles are emitted that linger in the air, rather than infection exclusively through heavy “droplets” from coughs or sneezes)

Screenshot of first two paragraphs of the report

University of Nebraska Study referenced in this letter:

I am uncertain wther the study referenced for this chart it was data collected for source control (my mask protects you) or as PPE (my mask protects me).

Social distancing should still be adhered to

The latest science explained:

https://youtu.be/BA2BOT3A70w

Source control: my mask protects you, your mask protects me

Still need to social distance (6ft.) though

And now: The viral social media meme:

Correlation does not prove causation, but it can give us a wink and a nudge.

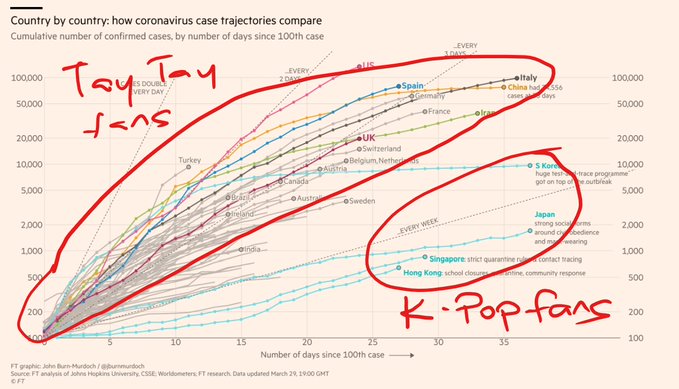

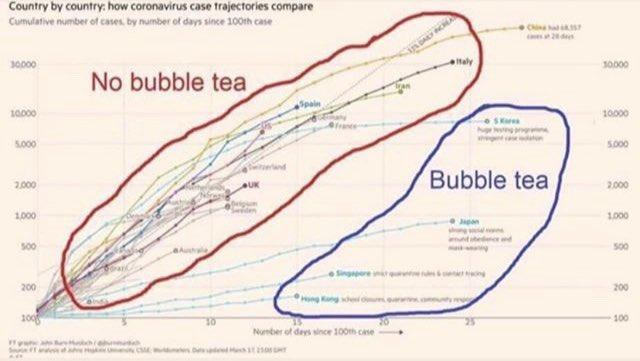

To be fair, these four countries have also undertaken different types of disease control to western countries in other ways (e.g. S Korea, Singapore with aggressive early response and lockdowns)

And, it’s thought that even if masks help, it would mostly be to protect others from yourself. Social distancing (6ft) still matters, and I would wager that even then it’s probably not a guarantee.

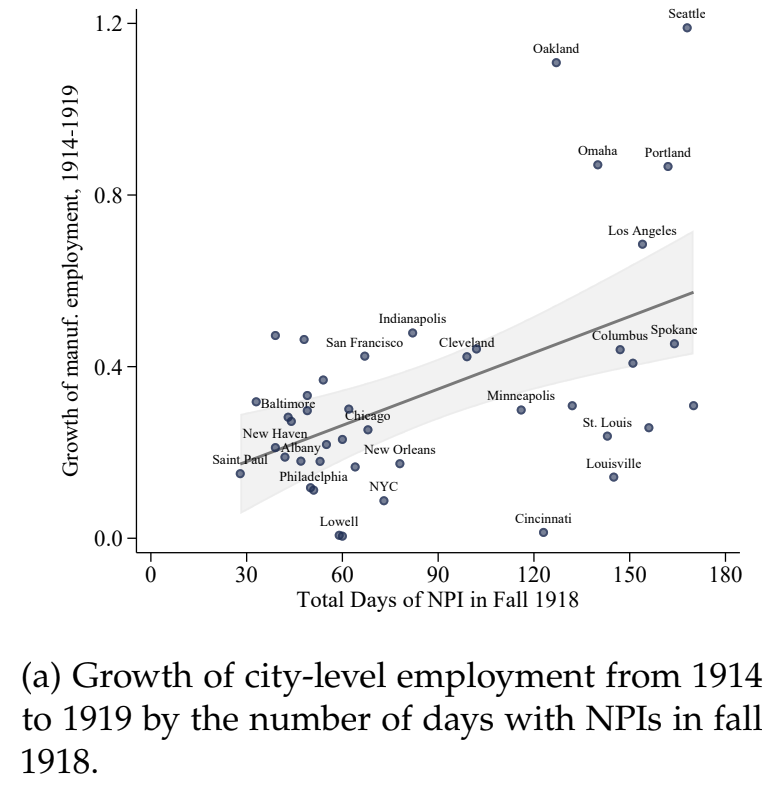

We find that cities that intervened earlier and more aggressively do not perform worse and, if anything, grow faster after the pandemic is over. Our findings thus indicate that NPIs not only lower mortality; they also mitigate the adverse economic consequences of a pandemic.

Matt’s note: a preliminary version of this paper (seeking comments) was released on March 26th that was used for the creation of this article.

The paper was published in full on June 6th, in which it re-affirmed its position as made in the March 26th preliminary publication.

The March 26th preliminary version has been replaced with the June 6th final publication for the preview above, but the original preliminary can be found here for comparison.

This paper examines the impact of 1918 Flu pandemic and resulting non-pharmaceutical interventions on real economic activity. Using variation across U.S. states and cities, we deliver two key messages.

First, the pandemic leads to a sharp and persistent fall in real economic activity. We find negative effects on manufacturing activity, the stock of durable goods, and bank assets, which suggests that the pandemic depresses economic activity through both supply and demand-side effects.

Second, cities that implemented more rapid and forceful non-pharmaceutical health interventions do not experience worse downturns.

In contrast, evidence on manufacturing activity and bank assets suggests that the economy performed better in areas with more aggressive NPIs after the pandemic.

Altogether, our evidence implies that pandemics are highly disruptive for economic activity. However, timely measures that can mitigate the severity of the pandemic can reduce the severity of the persistent economic downturn. That is, NPIs can reduce mortality while at the same time being economically beneficial.

More:

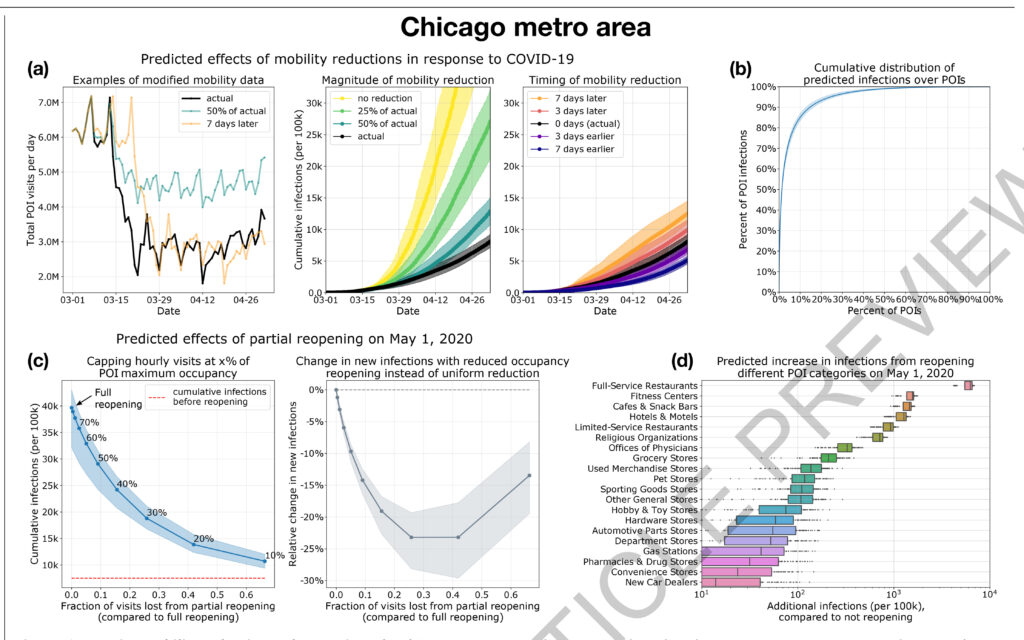

(Nature Research) Mobility network models of COVID-19 explain inequities and inform reopening

Derived from cell phone data, our mobility networks map the hourly movements of 98 million people from neighborhoods (census block groups, or CBGs) to points of interest (POIs) such as restaurants and religious establishments, connecting 57k CBGs to 553k POIs with 5.4 billion hourly edges. We show that by integrating these networks, a relatively simple SEIR model can accurately fit the real case trajectory, despite substantial changes in population behavior over time. Our model predicts that a small minority of “superspreader” POIs account for a large majority of infections and that restricting maximum occupancy at each POI is more effective than uniformly reducing mobility.

Matt’s Note:

Take note of the bar chart on the bottom right,

Its scale is exponential, meaning that items further right on the graph are modeled as spreading infection orders of magnitude more than those near the origin.

This may explain why these researchers’ model (based on rigorous use of cellphone data) suggests that targeted policies towards limiting infection spread at specific POI’s could have a profound impact in reducing the severity of the ongoing pandemic.