*most of the following is guesswork on my part, I don’t know this for certain

The triple whammy of lowering interest rates from central banks, cheapening oil prices as Russia and Saudi Arabia engage in a price war and dump cheap oil into markets, and wide impacts of the coronavirus could pose a serious threat to many of the world’s banks, especially those that have struggled with profit opportunities in the wake of perpetually low interest rates and leverage this past decade.

Generally, banks make money by charging people money to access their balance sheets. If they don’t charge enough, there can be problems. If lending rates are higher, they can fudge the numbers a bit more and make more money when dealing with large volumes of loans (at least, as I understand it).

If lending rates are lower, there can be problems.

The author also says that oil shortages in the 70’s caused supply shortages (and therefore inflation), but that current surpluses in oil will have deflationary pressures.

While this may be true, I don’t know if generalized supply shortages caused by the coronavirus could have a counteracting, or more effective inflationary pressure. Should be interesting to see.

These are interesting and historic times to be sure.

Edit: a further note:

I know next to nothing about macroeconomics, but just from what I’ve been watching on Bloomberg yesterday it seems like people are advocating for central banks to immediately drop interest rates to zero and pour dump trucks worth of cash on the emerging recession. I don’t quite know if this would be a good idea.

The stimulus done in ’08 was supposedly very effective, but it’s unclear whether the same could be said for this time around:

[I think this shows effectively how much money the fed prints (Quantitative Easing)]

Edit 2 (Wednesday): I heard someone saying on NPR this morning that even though fiscal stimulus is likely to be ineffective, it’s important for inverstor’s “feelings”.

This confirms my suspicions that U.S. economic planning (or lack thereof) has been “feelings” based rather than “preventing an obscene train wreck” based for quite some time.

People were quick to say how “well” the economy was doing with such low interest rates, but you can’t eat your cake and have it too. Eventually, you have to face reality.

In other words, candy may taste sweet, but if you eat too much of it, you’ll get sick.

We are calling on every country to act with speed, scale and clear-minded determination.

Although we continue to see the majority of cases in a handful of countries, we are deeply concerned about the increasing number of countries reporting cases, especially those with weaker health systems.

However, this epidemic is a threat for every country, rich and poor. As we have said before, even high-income countries should expect surprises. The solution is aggressive preparedness.

We’re concerned that some countries have either not taken this seriously enough, or have decided there’s nothing they can do.

We are concerned that in some countries the level of political commitment and the actions that demonstrate that commitment do not match the level of the threat we all face.

This is not a drill.

This is not the time to give up.

This is not a time for excuses.

This is a time for pulling out all the stops.

Countries have been planning for scenarios like this for decades. Now is the time to act on those plans.

…

(NYT) China’s Battle Against Coronavirus: 7 Takeaways

Do we know what this virus’s lethality is? We hear some estimates that it’s close to the 1918 Spanish flu, which killed 2.5 percent of its victims, and others that it’s a little worse than the seasonal flu, which kills only 0.1 percent. How many cases are missed affects that.

There’s this big panic in the West over asymptomatic cases. Many people are asymptomatic when tested, but develop symptoms within a day or two.

In Guangdong, they went back and retested 320,000 samples originally taken for influenza surveillance and other screening. Less than 0.5 percent came up positive, which is about the same number as the 1,500 known Covid cases in the province. (Covid-19 is the medical name of the illness caused by the coronavirus.)

There is no evidence that we’re seeing only the tip of a grand iceberg, with nine-tenths of it made up of hidden zombies shedding virus. What we’re seeing is a pyramid: most of it is above ground.

Once we can test antibodies in a bunch of people, maybe I’ll be saying, “Guess what? Those data didn’t tell us the story.” But the data we have now don’t support it.

——–2020-04-04 Matt’s Note: There has been more research and it seems asymptomatic trasnmission is likely———

That’s good, if there’s little asymptomatic transmission. But it’s bad in that it implies that the death rates we’ve seen — from 0.7 percent in parts of China to 5.8 percent in Wuhan — are correct, right?

I’ve heard it said that “the mortality rate is not so bad because there are actually way more mild cases.” Sorry — the same number of people that were dying, still die. The real case fatality rate is probably what it is outside Hubei Province, somewhere between 1 and 2 percent.

…

How did the Chinese reorganize their medical response?

First, they moved 50 percent of all medical care online so people didn’t come in. Have you ever tried to reach your doctor on Friday night? Instead, you contacted one online. If you needed prescriptions like insulin or heart medications, they could prescribe and deliver it.

But if you thought you had coronavirus?

You would be sent to a fever clinic. They would take your temperature, your symptoms, medical history, ask where you’d traveled, your contact with anyone infected. They’d whip you through a CT scan …

Wait — “whip you through a CT scan”?

Each machine did maybe 200 a day. Five, 10 minutes a scan. Maybe even partial scans. A typical hospital in the West does one or two an hour. And not X-rays; they could come up normal, but a CT would show the “ground-glass opacities” they were looking for.

(Dr. Aylward was referring to lung abnormalities seen in coronavirus patients.)

And then?

If you were still a suspect case, you’d get swabbed. But a lot would be told, “You’re not Covid.” People would come in with colds, flu, runny noses. That’s not Covid. If you look at the symptoms, 90 percent have fever, 70 percent have dry coughs, 30 percent have malaise, trouble breathing. Runny noses were only 4 percent.

The swab was for a PCR test, right? How fast could they do that? Until recently, we were sending all of ours to Atlanta.

They got it down to four hours.

How good were the severe and critical care?

China is really good at keeping people alive. Its hospitals looked better than some I see here in Switzerland. We’d ask, “How many ventilators do you have?” They’d say “50.” Wow! We’d say, “How many ECMOs?” They’d say “five.” The team member from the Robert Koch Institute said, “Five? In Germany, you get three, maybe. And just in Berlin.”

(ECMOs are extracorporeal membrane oxygenation machines, which oxygenate the blood when the lungs fail.)

Who paid for all of this?

The government made it clear: testing is free. And if it was Covid-19, when your insurance ended, the state picked up everything.

In the U.S., that’s a barrier to speed. People think: “If I see my doctor, it’s going to cost me $100. If I end up in the I.C.U., what’s it going to cost me?” That’ll kill you. That’s what could wreak havoc. This is where universal health care coverage and security intersect. The U.S. has to think this through.

What about the nonmedical response?

It was nationwide. There was this tremendous sense of, “We’ve got to help Wuhan,” not “Wuhan got us into this.” Other provinces sent 40,000 medical workers, many of whom volunteered.

In Wuhan, our special train pulled in at night, and it was the saddest thing — the big intercity trains roar right through, with the blinds down.

We got off, and another group did. I said, “Hang on a minute, I thought we were the only ones allowed to get off.” They had these little jackets and a flag — it was a medical team from Guangdong coming in to help.

…

Isn’t it possible only because China is an autocracy?

Journalists also say, “Well, they’re only acting out of fear of the government,” as if it’s some evil fire-breathing regime that eats babies. I talked to lots of people outside the system — in hotels, on trains, in the streets at night.

They’re mobilized, like in a war, and it’s fear of the virus that was driving them. They really saw themselves as on the front lines of protecting the rest of China. And the world.

A mathematician who studies the spread of disease explains some of the figures that keep popping up in coronavirus news.

We’ve seen all sorts of numbers for fatality rates. Does the latest estimate of 3.4 percent globally make sense?

Early on, people looked at total current cases and deaths, which, as I said, is a flawed calculation, and concluded that the case fatality rate must be 2 percent based on China data. If you run the same calculation on yesterday’s totals for China, you get an apparent CFR (case fatality rate) of near 4 percent. People are speculating that something is happening with the virus, where it actually is just this statistical illusion that we’ve known about from Day 1. I’d say on best available data, when we adjust for unreported cases and the various delays involved, we’re probably looking at a fatality risk of probably between maybe 0.5 and 2 percent for people with symptoms.

…

If you were the average person, what would you pay attention to — in terms of the news and the numbers?

One signal to watch out for is if the first case in an area is a death or a severe case, because that suggests you had a lot of community transmission already. As a back of the envelope calculation, suppose the fatality rate for cases is about 1 percent, which is plausible. If you’ve got a death, then that person probably became ill about three weeks ago. That means you probably had about 100 cases three weeks ago, in reality. In that subsequent three weeks, that number could well have doubled, then doubled, then doubled again. So you’re currently looking at 500 cases, maybe a thousand cases.

I think the other thing that people do need to pay attention to is the risk of severe disease and fatality, particularly in older groups, in the over-70s, over-80s. Over all we’re seeing maybe 1 percent of symptomatic cases are fatal across all ages. There’s still some uncertainty on that, but what’s also important is that 1 percent isn’t evenly distributed. In younger groups, we’re talking perhaps 0.1 percent, which means that when you get into the older groups, you’re potentially talking about 5 percent, 10 percent of cases being fatal.

I think most people aren’t aware of the risk of systemic healthcare failure due to #COVID19 because they simply haven’t run the numbers yet. Let’s talk math. 1/n

We’re looking at about 1M US cases by the end of April, 2M by ~May 5, 4M by ~May 11, and so on. Exponentials are hard to grasp, but this is how they go. 4/n

As the healthcare system begins to saturate under this case load, it will become increasingly hard to detect, track, and contain new transmission chains. In absence of extreme interventions, this likely won’t slow significantly until hitting >>1% of susceptible population. 5/n

What does a case load of this size mean for healthcare system? We’ll examine just two factors — hospital beds and masks — among many, many other things that will be impacted.

The US has about 2.8 hospital beds per 1000 people. With a population of 330M, this is ~1M beds. At any given time, 65% of those beds are already occupied. That leaves about 330k beds available nationwide (perhaps a bit fewer this time of year with regular flu season, etc). 7/n

Let’s trust Italy’s numbers and assume that about 10% of cases are serious enough to require hospitalization. (Keep in mind that for many patients, hospitalization lasts for *weeks* — in other words, turnover will be *very* slow as beds fill with COVID19 patients). 8/n

By this estimate, by about May 8th, all open hospital beds in the US will be filled. (This says nothing, of course, about whether these beds are suitable for isolation of patients with a highly infectious virus.) 9/n

If we’re wrong by a factor of two regarding the fraction of severe cases, that only changes the timeline of bed saturation by 6 days in either direction. If 20% of cases require hospitalization, we run out of beds by ~May 2nd. 10/n

If only 5% of cases require it, we can make it until ~May 14th. 2.5% gets us to May 20th. This, of course, assumes that there is no uptick in demand for beds from *other* (non-COVID19) causes, which seems like a dubious assumption. 11/n

In any crisis, leaders have two equally important responsibilities: solve the immediate problem and keep it from happening again. The Covid-19 pandemic is a case in point. We need to save lives now while also improving the way we respond to outbreaks in general. The first point is more pressing, but the second has crucial long-term consequences.

The long-term challenge — improving our ability to respond to outbreaks — isn’t new. Global health experts have been saying for years that another pandemic whose speed and severity rivaled those of the 1918 influenza epidemic was a matter not of if but of when.1 The Bill and Melinda Gates Foundation has committed substantial resources in recent years to helping the world prepare for such a scenario.

Now we also face an immediate crisis. In the past week, Covid-19 has started behaving a lot like the once-in-a-century pathogen we’ve been worried about. I hope it’s not that bad, but we should assume it will be until we know otherwise.

There are two reasons that Covid-19 is such a threat. First, it can kill healthy adults in addition to elderly people with existing health problems. The data so far suggest that the virus has a case fatality risk around 1%; this rate would make it many times more severe than typical seasonal influenza, putting it somewhere between the 1957 influenza pandemic (0.6%) and the 1918 influenza pandemic (2%).2

Second, Covid-19 is transmitted quite efficiently. The average infected person spreads the disease to two or three others — an exponential rate of increase. There is also strong evidence that it can be transmitted by people who are just mildly ill or even presymptomatic.3 That means Covid-19 will be much harder to contain than the Middle East respiratory syndrome or severe acute respiratory syndrome (SARS), which were spread much less efficiently and only by symptomatic people. In fact, Covid-19 has already caused 10 times as many cases as SARS in a quarter of the time.

People aren't surprised when I tell them there are 13,000 Covid-19 cases outside China, or when I tell them this number doubles every 3 days. But when I tell them that if growth continues at this rate, we'll have 1.7 million cases in 3 weeks, they're astonished.

Maintain at least 2 metres (6 feet) distance between yourself and anyone else.

Why? When someone coughs or sneezes they spray small liquid droplets from their nose or mouth which may contain virus. If you are too close, you can breathe in the droplets, including the COVID-19 virus if the person coughing has the disease.

Matt’s Note: While not currently known for certain, it is thought that it is also possible to pick up the virus from aerosolized particles that are emitted during breathing or speaking as well. These particles can also linger in the air after an infected person has left.

In addition, social distancing is important even amongst seemingly healthy people due the presence of asymptomatic carriers that can likely also pass on the virus via aerosols emitted during breathing or speaking.

Avoid touching eyes, nose and mouth

Why? Hands touch many surfaces and can pick up viruses. Once contaminated, hands can transfer the virus to your eyes, nose or mouth. From there, the virus can enter your body and can make you sick.

Practice respiratory hygiene

Make sure you, and the people around you, follow good respiratory hygiene. This means covering your mouth and nose with your bent elbow or tissue when you cough or sneeze. Then dispose of the used tissue immediately.

Why? Droplets spread virus. By following good respiratory hygiene you protect the people around you from viruses such as cold, flu and COVID-19.

Please also refer to more recent official public health releases, including details on the risks of aerosolized respiratory transmission, i.e. “Sharing the same air” in enclosed spaces.

Matt’s thoughts:

Covid-19 is no picnic (i.e. “a worse version of the flu”). Communities should make reasonable and proactive preparations accordingly.

Germs that jump species such as Covid-19 can be serious because they take a harder toll on the immune system of humans than that of the species the virus originated in:

Anyone doubting the seriousness of a potential pandemic need look no further than the 1918 Spanish Flu:

In the U.S., about 28% of the population of 105 million became infected, and 500,000 to 675,000 died (0.48 to 0.64 percent of the population)

I would like to make it so that readers can sign up to be notified of new posts via email on the Homepage or at the bottom of any post

An email should be sent out to the reader daily if new posts are created

The email should contain a list of the posts created since they were last notified, along with the HTML content of the latest post in the body of the email

The campaign should auto populate to Twitter as well

Make use of RSS newsfeed provided by Wordpress websites

Every Wordpress website provides an RSS newsfeed at example.com/feed in a standard format

This feed contains the titles, dates, and contents of the website's posts

By telling Mailchimp to monitor it, we can set up an automation to send out an email and post to Twitter whenever a new post is created

Creating a Mailchimp RSS Campaign:

Create a new campaign

Search for "RSS" and create an "RSS" or "Blog" campaign

Input the feed URL provided by our Wordpress site to Mailchimp

Email to the whole list

Personalize our campaign info, customized using the merge tag *|RSSFEED:DATE|* to inform and entice the reader

Set up an auto Twitter post, customized using the RSS merge tag *|RSS:RECENTxxx|*. xxx is a number, in our case 10 indicating that the 10 newest posts since the last email was sent will be included. They will show up as hyperlinks where the text is the title of the posts.

Select the full width campaign template for more space

Now we customize our email template

Greeting for the user in text:

Hello, *|IF:EMAIL ! <<Email Address>>|**|EMAIL|**|ELSE:|*friend*|END:IF|*, You may be interested in new article(s) I've written on my website, matthew.krupczak.org:

In my signup form, I only ask for an email address (and not first name / last name) in order to reduce user friction.

If a user is reading the campaign in email, it would be nice to mention their email address specifically so they know it's not mass spam.

If a user is viewing the campaign page from Twitter, no email address will be available. We can greet them as 'friend' instead

If the user's email address is not a placeholder from Mailchimp's software, print the user's email. Else, print "friend".

Let's look at our template again:

*|RSS:RECENTxxx|*. xxx is a number, in our case 10 indicating that the 10 newest posts since the last email was sent will be included. They will show up as hyperlinks where the text is the title of the posts.

RSS Merge Tags are included directly after this which will show the title, date of publication, and full HTML content of the latest post on my website

Dynamic Social Cards:

To inform and entice the reader, I use a RSS Merge Tag to include the date and title of my most recent post

There was a time when the primary role of leaders at most companies was management. The technology required to do the work of a company could be bought or siloed in an “IT department,” treated more as a cost center than a source of competitive advantage.

Walmart is a good case study in how to bring on technical co-founders, even when your company is already worth hundreds of billions of dollars and employs nearly as many people as the People’s Liberation Army.

…

Mr. Lore is now chief of e-commerce at Walmart. A remarkable number of his lieutenants have also stayed on and been promoted to leadership roles within the company. Walmart’s e-commerce business revenue grew 43% in the last quarter alone. By all appearances, the company that is to this day based in its original hometown of Bentonville, Ark., is successfully pursuing a “second-mover strategy” against its much more highly valued competitor in Seattle.

…

As the competitive landscape continues to change and technology becomes ever more essential to how business is done, investments that might have seemed too risky a few years ago now may sometimes turn out to be the best path to survival.

“There is an existential threat to Fortune 500 companies before the end of this decade,” says Mr. O’Sullivan, the angel investor. “You can actually see companies that are less than 10 years old knocking off and surpassing companies which have been around for 100 years.”

It is too soon to predict the long-run arc of the coronavirus outbreak. But it is not too soon to recognise that the next global recession could be around the corner – and that it may look a lot different from those that began in 2001 and 2008.

For starters, the next recession is likely to emanate from China, and indeed may already be under way. China is a highly leveraged economy, it cannot afford a sustained pause today anymore than fast-growing 1980s Japan could. People, businesses and municipalities need funds to pay back their out-size debts. Sharply adverse demographics, narrowing scope for technological catch-up, and a huge glut of housing from recurrent stimulus programmes – not to mention an increasingly centralised decision-making process – already presage significantly slower growth for China in the next decade.

…

Moreover, unlike the two previous global recessions this century, the new coronavirus, Covid-19, implies a supply shock as well as a demand shock. Indeed, one has to go back to the oil-supply shocks of the mid-1970s to find one as large. Yes, fear of contagion will hit demand for airlines and global tourism, and precautionary savings will rise. But when tens of millions of people can’t go to work (either because of a lockdown or out of fear), global value chains break down, borders are blocked, and world trade shrinks because countries distrust of one another’s health statistics, the supply side suffers at least as much.

…

But policymakers and altogether too many economic commentators fail to grasp how the supply component may make the next global recession unlike the last two. In contrast to recessions driven mainly by a demand shortfall, the challenge posed by a supply-side driven downturn is that it can result in sharp declines in production and widespread bottlenecks. In that case, generalised shortages – something that some countries have not seen since the gas queues of 1970s – could ultimately push inflation up, not down.

…

The odds of a global recession have risen dramatically, much more than conventional forecasts by investors and international institutions care to acknowledge. Policymakers need to recognise that, besides interest rate cuts and fiscal stimulus, the huge shock to global supply chains also needs to be addressed. The most immediate relief could come from the US sharply scaling back its trade-war tariffs, thereby calming markets, exhibiting statesmanship with China, and putting money in the pockets of US consumers. A global recession is a time for cooperation, not isolation.

U.S. Dollar weakness is a foremost concern of mine. As such, I have extensively written about it. I am very concerned that the actions being taken to “improve” our economic situation will dramatically weaken the Dollar. Should the Dollar substantially decline from here, as I expect, the negative consequences will far outweigh any benefits. The negative impact of a substantial Dollar decline can’t, in my opinion, be overstated. The following three charts illustrate various technical analysis aspects of the U.S. Dollar, as depicted by the U.S. Dollar Index. First, a look at the monthly U.S. Dollar from 1983. This clearly shows a long-term weakness, with the blue line showing technical support until 2007, and the red line representing a (past) trendline: (charts courtesy of StockCharts.com; annotations by the author) (click on charts to enlarge images)

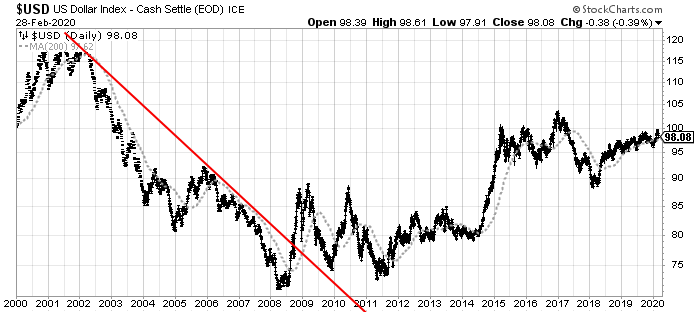

– Next, another chart, this one focused on the daily U.S. Dollar since 2000 on a LOG scale. The red line represents a (past) trendline. The gray dotted line is the 200-day M.A. (moving average):

– Lastly, a chart of the Dollar on a weekly LOG scale. There are two clearly marked past channels, with possible technical support depicted by the dashed light blue line:

– I will continue providing updates on this U.S. Dollar situation regularly as it deserves very close monitoring…

In any crisis, leaders have two equally important responsibilities: solve the immediate problem and keep it from happening again. The Covid-19 pandemic is a case in point. We need to save lives now while also improving the way we respond to outbreaks in general. The first point is more pressing, but the second has crucial long-term consequences.

The long-term challenge — improving our ability to respond to outbreaks — isn’t new. Global health experts have been saying for years that another pandemic whose speed and severity rivaled those of the 1918 influenza epidemic was a matter not of if but of when.1 The Bill and Melinda Gates Foundation has committed substantial resources in recent years to helping the world prepare for such a scenario.

Now we also face an immediate crisis. In the past week, Covid-19 has started behaving a lot like the once-in-a-century pathogen we’ve been worried about. I hope it’s not that bad, but we should assume it will be until we know otherwise.

There are two reasons that Covid-19 is such a threat. First, it can kill healthy adults in addition to elderly people with existing health problems. The data so far suggest that the virus has a case fatality risk around 1%; this rate would make it many times more severe than typical seasonal influenza, putting it somewhere between the 1957 influenza pandemic (0.6%) and the 1918 influenza pandemic (2%).2

Second, Covid-19 is transmitted quite efficiently. The average infected person spreads the disease to two or three others — an exponential rate of increase. There is also strong evidence that it can be transmitted by people who are just mildly ill or even presymptomatic.3 That means Covid-19 will be much harder to contain than the Middle East respiratory syndrome or severe acute respiratory syndrome (SARS), which were spread much less efficiently and only by symptomatic people. In fact, Covid-19 has already caused 10 times as many cases as SARS in a quarter of the time.

Until this week, the market reaction to the virus had been mild — after a dip in late January, US and global equities rallied to new highs. This complacency was based on a number of flawed assumptions. First, that the epidemic would be limited mostly to China, rather than becoming a global pandemic. Second, that it would be contained and peak before the end of the first quarter, thus limiting the economic damage to China and the global economy. Third, that the growth path would be V-shaped, with a strong rebound in the second quarter and beyond. Fourth, that policymakers — both monetary and fiscal — would take strong early actions to support economies and markets, if things were to weaken significantly.

….

Assuming that China will rebound at this rate in the final three quarters of the year — which would imply growth in 2020 of 4 per cent — is heroically optimistic. It is more likely that a V-shape shows growth returning to a pre-virus annualised level of 6 per cent from the second quarter onwards. In this case, China’s calendar-year growth would be 2.5 per cent. Compare both the rosy and more realistic scenario with current market expectations, which have revised growth estimates for China from 6 per cent to 5.5 per cent, and you can see how investors are still delusional. An annual growth rate in the range of 2.5-4 per cent would also be a major shock to global growth and to other economies.

“”The expectation that policymakers will rapidly come to the rescue is also misguided. Fiscal policy will react very slowly, or not at all, given political and other constraints. Central banks are running out of bullets: how much more negative can the European Central Bank, Bank of Japan and others go on interest rates?

The US Federal Reserve has only 1.5 percentage points of headroom left. It will probably react in the second quarter by cutting rates, leading to short-term market relief. But this coronavirus outbreak is mostly a negative supply shock that reduces growth and increases costs and inflation, with some side-effects for aggregate demand. Monetary policy cannot resolve this.

…

The coronavirus outbreak is likely to be only one of many negative shocks that will hit the global economy this year. Others include the risk of a war between US and Iran causing a spike in oil prices; political chaos in the US as foreign rivals interfere in the upcoming election; and an escalation in tensions between US and China. Take all of this together, and the risk of a global recession is rising.””

While it’s true that the market always goes up in the long run, this is only true in the very long term. There have been multiple periods in the S&P’s history of many years with no appreciation.

My crazy ramblings:

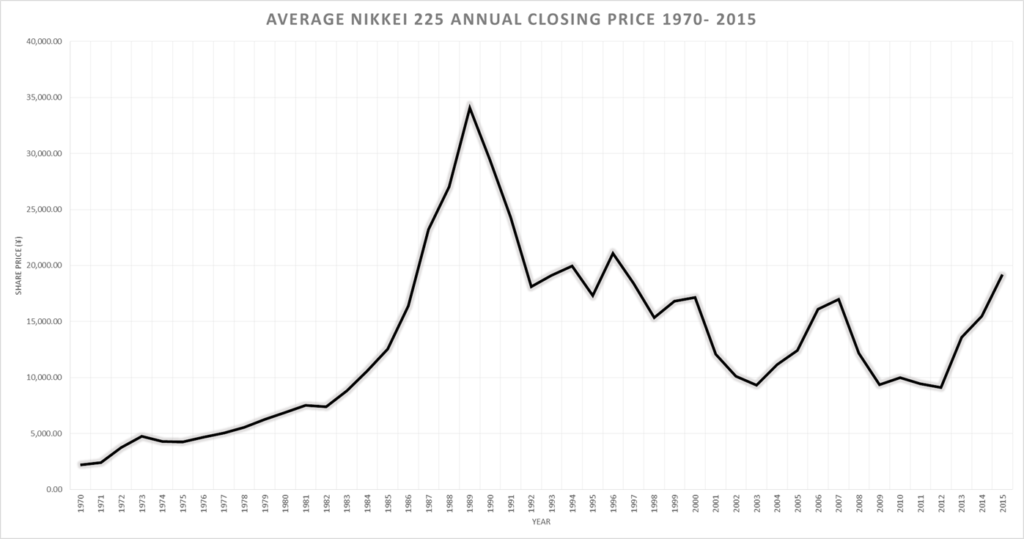

When Japan’s asset bubble burst in the 90’s, for various reasons their economy went mostly sideways until 2010. We could see something similar after this upcoming (…great, average, …great-er?) recession.

Japan’s strong economic growth in the second half of the 20th century ended abruptly at the start of the 1990s. The Plaza Accord doubling of the exchange rate value of the dollar versus the yen between 1985 and 1987 fueled a speculative asset price bubble of a massive scale. The bubble was caused by the excessive loan growth quotas dictated on the banks by Japan’s central bank, the Bank of Japan, through a policy mechanism known as the “window guidance”.[8][9] As economist Paul Krugman explained, “Japan’s banks lent more, with less regard for quality of the borrower, than anyone else’s. In doing so they helped inflate the bubble economy to grotesque proportions.”[10]

Eventually, many of these failing firms became unsustainable, and a wave of consolidation took place, resulting in four national banks in Japan. Many Japanese firms were burdened with heavy debts, and it became very difficult to obtain credit. Many borrowers turned to sarakin (loan sharks) for loans. As of 2012, the official interest rate was 0.1%;[14] the interest rate has remained below 1% since 1994.[15]

Nikkei 225 annual closing price saw the price sliding from 1990 onwards

This isn’t a reason to panic sell, and it isn’t even conclusive really, call it more a hunch than anything.

But Japan’s bubble burst showed: interest rates kept too low too long can cause an asset bubble to form, and once it pops, it’s extremely hard to crawl out of that hole.

The problem is: already too-low interest rates can’t reasonably go below zero. If they were to go below zero, lenders would receive less money back than they issued. This would make no sense: you’d be better off keeping money under your mattress than lending out.

It’s basic math. You’re stuck.

In Japan’s case, firms became less willing to take on debt, and productivity across the country didn’t increase much.

We may be in for a bumpy ride the next few years, but:

At this point, holding on to your assets, not panic selling, ignoring the news, and sitting and waiting is an arguably valid strategy

The market has been detached from economic fundamentals for a very long time. With central banks pumping unlimited liquidity over the last decade, which has nowhere to go (not too many worthy investment projects) the money has instead pilled in equities. Overvalued stocks only have one way to go and that is down. The trigger doesn’t need to be something attached to economic fundamentals either. It could be totally random, but broadly speaking it has to be something with global implications regardless of its overall magnitude. We shouldn’t blame the virus for triggering this. The market had it coming for a while.

.png)

.png)

.png)

.png)

.png)